For Struggling Tuition-Dependent Private Colleges: It’s Basic Economics

First Published on Stevens Strategy Blog

Michael K. Townsley, Ph.D., Senior Associate Stevens Strategy

Prefatory Remarks

Notices of private colleges closing or merging have become regular items in the press. However, this sudden spate of bad news may not be entirely due to new problems or to the effects of COVID. Rather, long-term financial issues may have been masked by massive doses of Covid aid; and now that COVID aid (i.e., HEERF Funding) has ended, the long-term problems have resurfaced.

The most vulnerable colleges in the current economic environment are private non-profit colleges with a tuition-dependency rate greater than 80% (a 60% tuition-dependency rate typically signifies that a college is mainly dependent on tuition for revenue. An 80% tuition-dependency rate suggests that a college has a very small endowment and donations represent a small portion of total revenue.). Before the pandemic. 22% of private non-profit colleges had a tuition-dependency rate greater than 80%, according to data from IPEDS (Integrated Postsecondary Education Data System).

The survival of private colleges and universities with high rates of tuition-dependency is subject to how well they manage the basic economic duality of supply and demand in relation to the market price for tuition. When an institution gets crossways with market forces like supply, demand, and price, it may not generate sufficient cash to cover its everyday expenses.

As Richard Garrett, Chief Research Officer at Eduventures, recently said,

“The problem is that all these [basic economic] trends (demographics, lost revenue, higher costs) aren’t going to get any better anytime soon. [For instance], the demographics are only going to get worse over the long-term.”

Basic Economics

Demand

For tuition-dependent private colleges, the key threat is the falling birth rates since the year 2000. Falling birth rates have led to a smaller pool of prospective student pools, and the pool is projected to continue to contract for the remainder of this decade. A shrinking prospective-student pool means tougher price completion and greater threats to tuition-dependent colleges.

Table I

Degree Seeking Students at 4-year Private Non-profit Institutions

|

Total (thousands) |

Change |

% Change |

|

|

2017 |

2,554 |

||

|

2018 |

2,548 |

-6.0 |

-0.2% |

|

2019 |

2,524 |

-24.0 |

-0.9% |

|

2020 |

2,494 |

-30.0 |

-1.2% |

|

2021 |

2,465 |

-29.0 |

-1.2% |

|

2022 |

2,448 |

-17.0 |

-0.7% |

|

Total Change |

-106.0 |

-4.2% |

|

Table I from the National Student Clearinghouse shows that enrollments steadily declined for undergraduate degree-seeking students between 2017 and 2022. From 2017 to 2022, 106,000 fewer students enrolled resulting in a loss of a sizeable amount of revenue and cash from tuition.

National Student Clearinghouse data (SEE Table II) also shows that no region of the country was spared from declining enrollments. Post-COVID in 2021, enrollment declines continued except for the West where enrollments increased. The pace of the fall in enrollments improved in 2022 except for the South, which reported a small increase, and the West, where enrollments abruptly decreased by its highest level in the past five years. Projected enrollment trends suggest improving conditions for enrollment; but based upon market factors (such as cost, perceived need for a college degree, and demographic shifts), it appears that enrollment increases will only be temporary before returning to a pattern of fewer students.

Table II

Changes in Total Enrollment (000) for Private Institutions 2017 to 2022

|

2018 |

2019 |

2020 |

2021 |

2022 |

Total |

|

|

Midwest |

(147) |

(60) |

(182) |

(81) |

(38) |

(508) |

|

Northeast |

(82) |

(53) |

(122) |

(92) |

(16) |

(365) |

|

South |

(99) |

(19) |

(131) |

(144) |

10 |

(383) |

|

West |

(93) |

(17) |

(152) |

478 |

(624) |

(408) |

|

Nation |

(421) |

(149) |

(587) |

161 |

(668) |

(1,664) |

For tuition-dependent colleges, demand has been weakened by a nearly twenty-year- long drought in new births; and supply has been upset by students no longer selecting traditional liberal arts majors.

Ten years ago, evidence began to accumulate that college graduates were choosing careers that were not related to their majors. The Wall Street Journal reported “that colleges are separating into winners and losers because students are rejecting colleges which consistently ranked low in preparing students for work.” The majors with the highest levels of underemployment is when the average wage for a graduate is less than the average wage for all college graduates). The underemployed majors were: psychology, visual and performing arts, and the social sciences. The federal government is well aware of this deficit and is likely to mandate that all schools provide to prospective students a program-level report of employability for their graduates, likely in an effort to reduce student loan debt moving forward.

Net Price

Usually, the relative balance of demand and supply among competitors determines price. The current state of demand in higher education has unbalanced the demand and supply relationship, especially for tuition-dependent institutions that have seemingly lost control of pricing. Therefore, we will discuss price or tuition before we consider the supply part of the basic economic duality.

Price in higher education, in particular among tuition-dependent colleges and universities, consists of two components – posted tuition and net price. The posted tuition is the amount that institutions typically present as the full-cost for enrollment. Net Price, on the other hand, is the amount paid by the student after deducting unfunded institutional and other financial aid (loans are not a form of financial aid because they must be repaid). Net price is the amount of tuition remaining after unfunded institutional aid (tuition discount) is deducted.

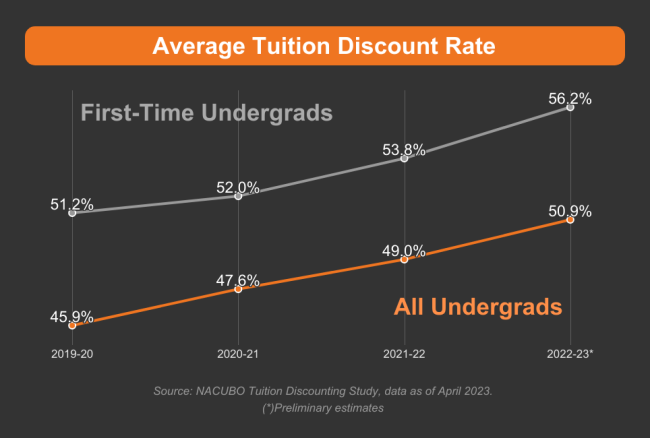

Unfortunately for tuition-dependent colleges, as the prospective student market erodes, there is ever-greater pressure by competitors to increase tuition discounts leading to ever-smaller levels of net tuition (See Chart I). Today, some colleges are already offering tuition discounts of 70% or more of the posted tuition. High tuition discount rates barely leave enough cash to make payroll and cover their outstanding bills.

Chart I

NACUBO Chart on Tuition Discounts

As Kenneth Redd, Director of Research and Policy Analysis at NACUBO, has stated,

“There are two reasons for the [current and future] escalation [in tuition discounting.] ‘One is that the competition for students now has become extremely fierce,’ he says. ‘[And with] birthrates steadily falling, fewer young people are applying to college. The second reason: more families are financially strapped.’

Supply

Supply is the product or service offered by an organization to prospective buyers. For tuition-dependent private colleges, the product typically is an academic degree. The decision for the board of trustees and president is how much supply to offer and the net price (net tuition) to offer students in the marketplace.

It is all too obvious that larger tuition (price) discounts are not yielding larger enrollments. Tuition discounting has become a losing strategy. As William Hall, President of Applied Policy Research, has noted,

“If you want to grow [and survive], you’re going to have to do something [distinctive] to induce additional yield.”

A survey in 2019 indicated that 27% of college graduates regretted choosing a humanities major (i.e., liberal arts major). By 2022 the percentage of graduates with regrets about choosing a humanities degree had increased to 48%. Buyer’s remorse of nearly 50% can have a spillover effect to prospective students, who are also looking for majors more directly connected to future employment. When graduates in the liberal arts disciplines express this level of dissatisfaction, it will further depress the market for liberal arts programs. Dissatisfaction among current students is also evidenced by attrition. Attritted students are not returning to college as they once did, regardless of the blandishments offered (Examples of blandishments include: large discounts, on-line courses, counseling, payment alternatives, loan restructuring, and other offers that admission and marketing officers have devised.)

Of considerable concern to private colleges chiefly offering liberal arts or humanities degrees is that high school graduates are moving away from those majors and seeking more practical job-oriented degrees or even opting for certificates or other non-degree options to improve their value in the work force. None of these bode well for the future of private liberal arts colleges.

With fewer prospective students choosing liberal arts or humanities majors, tuition-driven liberal arts college are bearing the burden of over-investment in fixed capital assets (buildings and furnishings) and faculty assigned and tenured in these programs. Moreover, the liberal arts faculty, especially tenured faculty, are not easily moved into new programs such as offering degrees in business or technology. Additionally, when students do not attain a liberal arts degree, it causes a second-level problem. In the past, 40% of liberal arts graduates went on for an advanced degree (e.g., philosophy bachelor’s degree graduates would earn a master’s in philosophy), which generated more tuition revenue.

Transforming a liberal arts college into a more career-oriented institution can have profound challenges because the institution is overly invested in degrees that prospective students no longer want. However, an article from Inside Higher Education in 2012 pointed out that some liberal arts colleges, though keeping liberal arts in their mission, were moving their curriculum toward more practical workplace applications.

One of the primary strategies for a supplier operating in an intensely price-competitive marketplace, is to differentiate themselves from their competitors. Colleges and universities have introduced multiple strategies over the years to differentiate themselves from their competitors. Here are several examples of differentiation strategies used by tuition-dependent colleges: block scheduling, new academic programs, schedules that accommodated working students, easing transfer credit rules, opening off-site instructional programs, contracting special discounts to groups of students (e.g., a cohort of law enforcement officers), online programs, and offering college credit courses to high school students. The most recent and almost universally example of colleges responding to changes in the marketplace is when the pandemic forced colleges without online courses to quickly install the online technology or lose their students. What will tuition-dependent colleges do in the future to expand revenue flows? That will depend on how quickly a president can see new opportunities, which are dependent on location, flexibility of the institution, and access to financial resources.

Besides the differentiation of products and services, there is one other significant option — cut the cost of producing the product. Cutting cost reduces upward pressure on pricing. Most colleges find this option the most difficult to implement because of internal (faculty, students, athletic programs, etc.) and external (alumni, government regulations, donors, etc.) constraints. Yet, college presidents and boards of trustees must understand that when costs per student rise faster than the income from prospective student, they will never get control of an institutional pricing strategy or of its long-term financial viability.

For tuition-dependent institutions looking to respond effectively to the demands of the market, Stevens Strategy has developed Chronos UniversityTM., a revolutionary design for the university of the future. It meets the needs of tuition-dependent institutions: It lower their costs of operation by maximizing faculty effectiveness, responds to the expectations of the new generation of students by creating opportunities for a consistent, personalized experience, applies technology to enhance instruction, and places the university in a distinctive position in its market by taking a unique, student-focused approach to higher education.

The Chronos concept integrates technology-based instruction with on-site or remote small group projects and daily face-to-face interaction with learning coaches to promote student learning and success. Chronos UniversityTM is designed to revolutionize the delivery of high-quality liberal arts and pre-professional undergraduate education. Interested readers can learn more about Chronos here.

Summary

Tuition-dependent colleges need to be keenly aware of their competitors and the goals and abilities of their prospective students. In the past, private colleges could offer a new way of differentiating themselves from the competitive herd, and it would take several years for the competition to react and to offer the same thing. During this period, a college could design new products or services and generate positive cash flow that strengthened its financial base. In today’s higher education marketplace, competitors will quickly react when another institution offers a program that enrolls a large number of new students spawning more revenue. Competitors will quickly replicate those programs because they are also desperate for new revenue sources.

When an institution is out-of-balance with market forces, it must act promptly to rebalance its relationship with the market. The college will need to speedily innovate or lose its capacity to survive. Presidents and boards of trustees of tuition-dependent colleges need to recognize that survival and success in their market depends on the interaction of demand and supply on the price of tuition, on their competitors and their goals and plans, on the income of prospective students and their capacity to pay the tuition bill, and on the students and/or families to see a payoff from tuition debt.

As is evident to anyone working or knowledgeable of higher education, declining enrollments combined with the other fundamentals (such as student preferences for an academic degree, net price, inflation, and unexpected expenses or situations like COVID) are pushing many private colleges to the precipice of failure.

As noted at the very start of this article, economic conditions are forcing some non-profit private colleges to merge or to close. (This is what happens in the business sector when a sector of the business market can no longer sustain revenues to cover expenses. For example, online catalogue stores and monster big box stores destabilized traditional retail operations.) Presidents can be continually on the lookout for strategic partnerships, like articulation agreements, or merger opportunities since one might emerge that makes sense. Merger partners should be considered before the school spirals too far down and has no value to a potential partner. Finally, trustees may determine that they do not want to modify the institutional mission to meet the market or that the institution has no long-term financial viability and decide that closing the school is the best option. A school closing should be considered early so students, employees and vendors are not left in a lurch.

Boards and presidents need to seriously evaluate a school’s financial position and review strategies — realistic increased revenue opportunities, expense reductions, merger partners, and closing plans. A fiscally-prudent board of trustees at a tuition-dependent private college must get a grip on the condition of the institution that they are charged with overseeing. Otherwise, the future of the college and its responsibilities to its students may slip out of their hands.

PUBLICATION NOTES

N.B.; these notes are from the original paper. The original location of the endnote numbers in the body of the paper were removed due to issues with publication on the Blog Site. If you desire an original copy of the paper; contact mtown@dca.net

Moore, Keller (September 8, 2022); (Retrieved May 12, 2023); “Did you know? College closures are on the rise”; The James G. Martin Center for Academic Renewal; Did You Know? College Closures Are On the Rise — The James G. Martin Center for Academic Renewal (jamesgmartin.center).

Integrated Postsecondary Education Data Systems (Retrieved April 2023); “Robust SS Stress Test”; The Integrated Postsecondary Education Data System.

Burns, Hilary (April 28, 2023); (Retrieved May 12, 2023); “Why the business of small colleges no longer adds up”; Boston Globe; Why the business of small colleges no longer adds up (msn.com).

National Student Clearinghouse Research Center (February 2, 2023); (Retrieved May 12, 2023); “Table 1: Enrollment by Credential Level and Sector 2017-2022”; Current Term Enrollment Estimates | National Student Clearinghouse Research Center (nscresearchcenter.org).

Ibid; Current Term Enrollment Estimates | National Student Clearinghouse Research Center (nscresearchcenter.org).

Grawe, Nathan (January 4, 2020); “Demographics, demands, and destiny: Implications for the health of independent institutions”; 2020 Annual Meeting of the Council of Independent Colleges; slide 14.

National Student Clearinghouse Research Center (February 2, 2023); (Retrieved May 12, 2023); “Table 2: Total Region Enrollment 2017-2022”; Current Term Enrollment Estimates | National Student Clearinghouse Research Center (nscresearchcenter.org).

Schwartz, Natalie (May 23, 2023); (Retrieved May 23, 2023); “Bain warns of ‘perilous environment’ for colleges as COVID 19 relief dries up”; Bain warns of ‘perilous environment’ for colleges as COVID-19 relief dries up | Higher Ed Dive.

Hill, Cary (June 27, 2019); (Retrieved May 24, 2023); “This the most regrettable college major in America”; Market Watch; This is the most regrettable college major in America – MarketWatch. Plumer, Brad (May 20, 2013); (Retrieved May 15, 2023); “Only 27% of college graduates have a job related to their major; The Washington Post; https://www.washingtonpost.com/news/wonk/wp/2013/05/20/only-27-percent-of-college-grads-have-a-job-related-to-their-major/?utm_term=.bb8684d901e4. Belkin, Douglas (February 21, 2018); (Retrieved April 28, 2023); “U.S. colleges are separating into winners and losers”; The Wall Street Journal.

Cooper, Preston (June 8, 2018); Retrieved May 15, 2023); Underemployment persists throughout college graduates’ careers”; Forbes; https://www.forbes.com/sites/prestoncooper2/2018/06/08/underemployment-persists-throughout-college-graduates-careers/#547d9a087490.

Adams, Susan (May 20, 2021); (Retrieved May 12, 2023); “Colleges are discounting tuition more than ever”; Forbes; Private Colleges Are Discounting Tuition More Than Ever (forbes.com).

Ibid; Forbes; Private Colleges Are Discounting Tuition More Than Ever (forbes.com).

Moody, Josh (April 25, 2023); (Retrieved May 12, 2023); “Tuition discount rates hit new high”; Inside Higher Education; NACUBO study finds tuition discount rates at all-time high (insidehighered.com).

Hill, Cary (June 27, 2019); (Retrieved May 24, 2023); “This the most regrettable college major in America”; Market Watch; This is the most regrettable college major in America – MarketWatch.

Drozdowski, Mark (September 29, 2022); (Retrieved May 24, 2023); “College grads regret majoring in humanities fields”; Best Colleges.com; College Grads Regret Majoring in Humanities Fields | Best Colleges.

National Student Clearinghouse Research Center (April 25, 2023); (Retrieved May 14, 2023); “Some college, no credential”; Some College, No Credential | National Student Clearinghouse Research Center (nscresearchcenter.org).

Ezarik, Melissa (March 20, 2022); (Retrieved May 14, 2023); “Students approach admissions strategically and practically”; National Student Clearinghouse Research Center; Survey: Student college choices both practical and strategic (insidehighered.com).

Barshay, Jill (November 22, 2021); (Retrieved May 14, 2023); “The number of college graduates drop for the eight straight year”; Hechinger Report; The number of college graduates in the humanities drops for the eighth consecutive year | American Academy of Arts and Sciences (amacad.org).

Ibid; Hechinger Report; The number of college graduates in the humanities drops for the eighth consecutive year | American Academy of Arts and Sciences (amacad.org).

Jaschik, Scott (October 10, 2012); (Retrieved May 24, 2023); “Disappearing liberal arts colleges; Inside Higher Education; Study finds that liberal arts colleges are disappearing (insidehighered.com).

Moore, Keller (September 8, 2022); (Retrieved May 12, 2023); “Did you know? College closures are on the rise”; The James G. Martin Center for Academic Renewal; Did You Know? College Closures Are on the Rise — The James G. Martin Center for Academic Renewal (James martin. center).

Integrated Postsecondary Education Data Systems (Retrieved April 2023); “Robust SS Stress Test”; The Integrated Postsecondary Education Data System.

Burns, Hilary (April 28, 2023); (Retrieved May 12, 2023); “Why the business of small colleges no longer adds up”; Boston Globe; Why the business of small colleges no longer adds up (msn.com).

National Student Clearinghouse Research Center (February 2, 2023); (Retrieved May 12, 2023); “Table 1: Enrollment by Credential Level and Sector 2017-2022”; Current Term Enrollment Estimates | National Student Clearinghouse Research Center (nscresearchcenter.org).

Ibid; Current Term Enrollment Estimates | National Student Clearinghouse Research Center (nscresearchcenter.org).

Grawe, Nathan (January 4, 2020); “Demographics, demands, and destiny: Implications for the health of independent institutions”; 2020 Annual Meeting of the Council of Independent Colleges; slide 14.

National Student Clearinghouse Research Center (February 2, 2023); (Retrieved May 12, 2023); “Table 2: Total Region Enrollment 2017-2022”; Current Term Enrollment Estimates | National Student Clearinghouse Research Center (nscresearchcenter.org).

Schwartz, Natalie (May 23, 2023); (Retrieved May 23, 2023); “Bain warns of ‘perilous environment’ for colleges as COVID 19 relief dries up”; Bain warns of ‘perilous environment’ for colleges as COVID-19 relief dries up | Higher Ed Dive.

Hill, Cary (June 27, 2019); (Retrieved May 24, 2023); “This the most regrettable college major in America”; Market Watch; This is the most regrettable college major in America – MarketWatch.

Plumer, Brad (May 20, 2013); (Retrieved May 15, 2023); “Only 27% of college graduates have a job related to their major; The Washington Post; https://www.washingtonpost.com/news/wonk/wp/2013/05/20/only-27-percent-of-college-grads-have-a-job-related-to-their-major/?utm_term=.bb8684d901e4.

Belkin, Douglas (February 21, 2018); (Retrieved April 28, 2023); “U.S. colleges are separating into winners and losers”; The Wall Street Journal.

Cooper, Preston (June 8, 2018); Retrieved May 15, 2023); Underemployment persists throughout college graduates’ careers”; Forbes; https://www.forbes.com/sites/prestoncooper2/2018/06/08/underemployment-persists-throughout-college-graduates-careers/#547d9a087490.

Adams, Susan (May 20, 2021); (Retrieved May 12, 2023); “Colleges are discounting tuition more than ever”; Forbes; Private Colleges Are Discounting Tuition More Than Ever (forbes.com).

Ibid; Forbes; Private Colleges Are Discounting Tuition More Than Ever (forbes.com).

Moody, Josh (April 25, 2023); (Retrieved May 12, 2023); “Tuition discount rates hit new high”; Inside Higher Education; NACUBO study finds tuition discount rates at all-time high (insidehighered.com).

Hill, Cary (June 27, 2019); (Retrieved May 24, 2023); “This the most regrettable college major in America”; Market Watch; This is the most regrettable college major in America – MarketWatch.

Drozdowski, Mark (September 29, 2022); (Retrieved May 24, 2023); “College grads regret majoring in humanities fields”; Best Colleges.com; College Grads Regret Majoring in Humanities Fields | Best Colleges.

National Student Clearinghouse Research Center (April 25, 2023); (Retrieved May 14, 2023); “Some college, no credential”; Some College, No Credential | National Student Clearinghouse Research Center (nscresearchcenter.org).

Ezarik, Melissa (March 20, 2022); (Retrieved May 14, 2023); “Students approach admissions strategically and practically”; National Student Clearinghouse Research Center; Survey: Student college choices both practical and strategic (insidehighered.com).

Barshay, Jill (November 22, 2021); (Retrieved May 14, 2023); “The number of college graduates drop for the eight straight year”; Hechinger Report; The number of college graduates in the humanities drops for the eighth consecutive year | American Academy of Arts and Sciences (amacad.org).

Ibid; Hechinger Report; The number of college graduates in the humanities drops for the eighth consecutive year | American Academy of Arts and Sciences (amacad.org).

Jaschik, Scott (October 10, 2012); (Retrieved May 24, 2023); “Disappearing liberal arts colleges; Inside Higher Education; Study finds that liberal arts colleges are disappearing (insidehighered.com).