by Michael K. Townsley | May 9, 2026 | Private Colleges & Universities in Crisis

In an April 2025 blog, I raised the question of whether or not tuition discounting (institutional grants) has run its course for college with enrollment less than 2,000 full-time-equivalent students. The blog used data up to 2023. Now, I have added IPEDS data from data to the analysis, The analysis looks at the effect that a 1% change in tuition discounting has on enrollment.

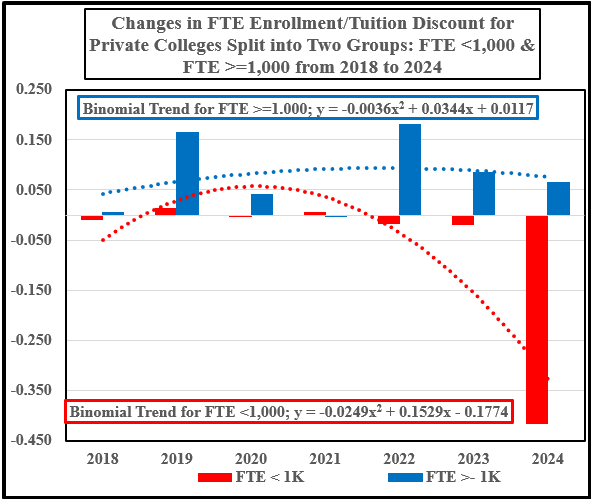

Chart 1 shows that for colleges with less than 2,000 students that any kind of a positive relationship between tuition discounting and enrollment has collapsed. Increasing the discount at these schools has had no impact on enrollment. It would almost appear that they have already encountered the demographic cliff five years before the predicted year. The polynomial trend suggests that calamity may be just around the corner.

For colleges with enrollments equal to or greater than 2,000 students, the polynomial trend suggests that the marginal value of tuition discounting may have started to flatten. It would not be too surprising that trend for these colleges will turn downward.

Chart 1

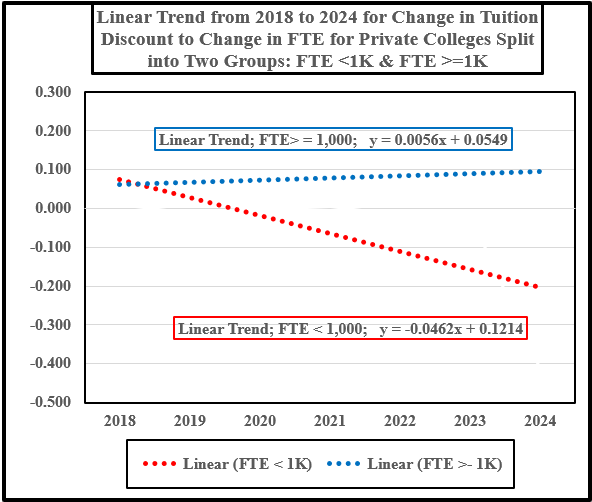

I have included Chart 2, which uses a linear trend analysis, because it is easier to interpret the slopes of a linear equation. Colleges with enrollments equal to or greater than 2,0000 students have a very small up ward trend, while the linear trend for colleges under 2,000 confirms what was noted for Chart 1. Small colleges are getting no effect from increases in tuition discounts.

Chart 2

For my conclusion, I will only talk about colleges with less than 2,000 FTE students. The average small college is wasting its time with tuition discounting. Here is an alternative pricing and by implication marketing strategy. If your college’s net tuition is less than the tuition charged by your competition, change your gross price so that it is under the competition. Then advertise that you offer students a quality degree with a reasonable price. If your net price is under the public university in your area, lower your price to slightly below the public university. Then advertise to their market that they can earn a degree at your college without the hassle of a major university that doesn’t care about you.

Wish you the best as you work to keep your college from tipping over the demographic cliff.

by Michael K. Townsley | Apr 25, 2026 | Private Colleges & Universities in Crisis

The Hechinger Report just published a study contending that “More Than 25% of Private Colleges Are at Risk of Closing.” This is a must read for every private college president and board member. Are you on the Hechinger List? Here is the citation: As one Vermont college finishes its last semester, a new projection shows that 442 more are at similar risk .

I, also, found the same potential for deep financial distress for private colleges in an analysis of 994 private colleges conducted three years ago.

The findings showed that 51 (5.4%) colleges faced a very high risk of closing within three years. These colleges had enrollments of less than 1,000 FTE students. Another 242 (25.5%) private colleges had a risk score placing them at great risk of closing within between three and six years. This risk band included colleges with enrollments between 1,000 and 2,000 FTE.

The analysis employed a Vulnerability Gauge based on a two variable logit regression that had an 86.3% prediction rate. The model used IPEDS data from the five-year period ending in 2024. My speculation is that as the slope of the demographic cliff increases many of the ‘great risk’ colleges will slide into the ‘high risk’ category.

The Hechinger Report and the Vulnerability Gauge need to be taken seriously by presidents and boards of trustees of private colleges. The window for taking strategic action will shrink quickly as each semester passes-by. When a college enters the Spring budget season, and if its risk continues to grow because enrollment and cash reserves are falling precipitously, the well-known strategy of ‘kicking the can down the road’ will no longer work. Under this strategy, the college could discover, all too soon, that the college has little or no financial reserves available to put an effective strategy into place.

by Michael K. Townsley | Apr 25, 2026 | Private Colleges & Universities in Crisis

The Wall Street Journal’s story about the struggles of St. Michael’s College is a must read for anyone who wants to understand the problems faced by colleges today and over the next decade. Ten years ago, no one would have believed that St. Michael’s would face long-term declines in enrollments and serial deficits. Now, it is, and its story is not an uncommon story for many colleges throughout the country.

Here is the citation: The Small Private Colleges Dying in a Winner-Take-All University Marketplace – WSJ

by Michael K. Townsley | Apr 25, 2026 | Private Colleges & Universities in Crisis

When Cutting Corners Becomes the Norm

Airlines, aircraft safety analysts, and organizational effectiveness managers use ‘normalizing operational deviance’ to describe when someone consistently violates policies and procedures until it becomes a standard method of operations. This concept often comes up when the National Transportation Safety Board (NTSB) reports on airplane accidents that were due to pilot negligence in not following standard procedures. For example, when a pilot in landing or take-off and makes too sharp a turn leading to a wing stall and the plane crashes. Another cases, is when an inexperienced private pilot fails to follow standard procedures during bad weather when landing at a busy commercial airport and crashes.

Non-aviation organizations are also susceptible to ‘normalizing operational deviance’, but there outcomes may not be as catastrophic as a plane wreck. Nevertheless, failing to follow procedures can result in strategic failures, overspending, violation of debt conditions, or significant accreditation problems.

Here are several examples of ‘normalizing deviance’ in colleges.

- Academic programs that do not closely monitor transcripts, which results in students graduating without earning the required credits. Both financial auditors and accreditors may catch this problem, and they can require the colleges to tell graduates that they did not accumulate sufficient credits to graduate and will then have to return to earn the missing credits. This is a very messy business because graduates do not want to return to classes, and they do not want to pay for the college’s mistake.

- President and chief academic officers that fail to develop rigorous operational plans to implement college strategies, which results in strategic expectations being dashed because critical steps were never taken. Over time, the chief leadership of the college assumes that all is well with their strategies until the plans fail leaving the college in deep financial and academic distress.

- Business offices too often pay for the purchases made by college employees who did not follow standard approval procedures. These unauthorized purchases can grow to a point where they lead to large budget over-runs. An unfortunate aspect of unauthorized purchases is that they distort budget and strategic plans by diverting financial resources to serve the interest of a department or an employee and not the college. By normalizing this deviant behavior, colleges are often surprised to discover that these unauthorized purchases are hard to control and can quickly deplete cash reserves.

- Equipment purchases are not tracked by the business office, which can lead to the loss of costly items. These losses often are not recognized until a fixed asset audit is conducted

- In some cases, presidents and chief buildings officers do not hire an independent construction manager to monitor construction so that the college can save money. The result is that they depend on the contractor to honestly follow speciation’s and regulations. If mistakes occur, material and design specifications are not followed, or local government building and zonings regulations are ignored, projects are delayed or expensive changes are needed, which result in cost overruns of the project. Long-term problems can show-up when equipment, materials, and sub-structures begin to fail. Even if the building is insured, insurance companies may reduce or reject claims because they believe the problems were caused by the negligence on the part of the college.

- IT can be problematic when the system is not set-up for consistent and regular backup, changes are not documented, the system is not updated, or system errors are allowed to linger and are not fixed.

In sum, normalizing operational deviance can lead to complacency, which could result in major system failures.

by Michael K. Townsley | Apr 25, 2026 | Private Colleges & Universities in Crisis

Slender Thread 4 deals with the outcome of the net revenue flows from enrollment to unrestricted net assets and finally to total net assets. The difference between unrestricted net assets and total net assets is that the first holds assets that can be converted to cash, though some unrestricted assets are not easily convertible and may even be devalued at the time of conversion, like receivables, inventory, and short-term assets tied to the bond market.

Net assets are the difference between total assets, which includes unrestricted assets, restricted endowments, and property; and liabilities, which includes bonds, notes, and other long-term loans. Beyond the information that we already have that unrestricted net assets are under stress, the issue is – are total net assets growing or shrinking in value before the full impact of the demographic crash?

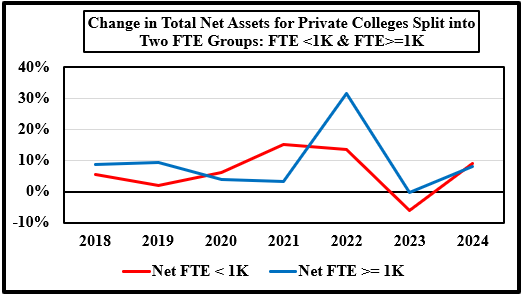

Chart 1 displays the change in total net assets between 2018 and 2024. This chart indicates that the six year period was a bumpy ride for small and large colleges. Total assets took their biggest hit in 2023, when the change in these assets took a big drop from large positive change in 2022 to a negative change. As was noted in the discussion on unrestricted net assets in Slender Thread – 3, the large influx of federal funds from COVID loans into unrestricted net assets carried over to total net assets. Then in 2023, the federal spigot closed, and the change in total net assets for small and large colleges dropped like a rock. The change in small college total assets slipped into negative change territory, while large colleges came within kissing distance of the zero-percentage line. In 2024, the change in total net assets bounced positive with small colleges reporting a greater change than did large colleges. Of course, the question remains – was the upward tick in 2024 indicative of long-term change in total net assets or was the change more like the up-down cycle between movements in 2019 and 2023 or the change could have been due to larger investment returns. In other words, will private colleges after 2024 return to the bumpy ride in total net assets that proceeded 2022? Charts 2 and 3 address long-term trends by using a linear and a second order polynomial to smooth the bumpy ride depicted in Chart 1.

Chart 1

- The data set includes 44 private colleges from IPEDS for the period 2017 to 2024 that offered a four-year degree subject to these exclusions because they have different business models: seminaries, yeshivas, art and music schools, research colleges, and colleges with missing data. The last year for the data is 2024; This set of colleges was split into two enrollment groups: FTE < 1,000 students and FTE >= 1,000 students. The data was then averaged for the two groups for each variable by year. The first chart has the basic data trend for both sets of private colleges, and the next two charts show the linear and a second-degree polynomial trend, i.e., a quadratic equation. ↑

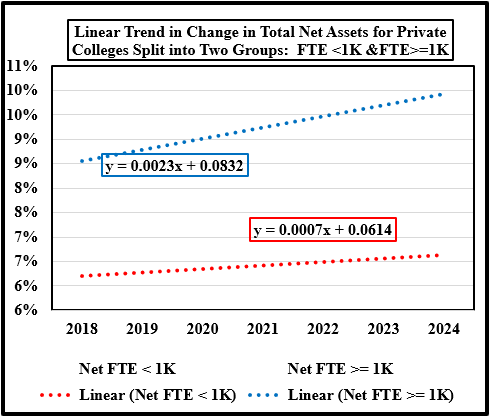

According to the linear trend in Chart 2; both small and large private colleges have a positive slope. However, the slope for small colleges is magnitudes less than the slope for large colleges. The slow rising slope for small colleges raises the question – will the change in the slope of these colleges turn negative and put the them in serious financial distress? Nevertheless, the trend in the rate of change remains above 6% for small colleges, which is a relatively strong trend over time.

Chart 2

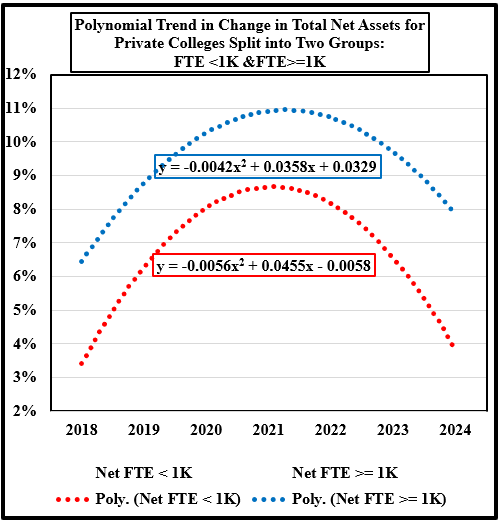

The polynomial trend in Chart 3 provides a different perspective than the linear trend in Chart 2. While the linear trends in Chart 2 iron out the bumps with a rising trend for both college groups, the polynomial trend in Chart 3 depicts a parabolic structure that rises through 2022 for large colleges and through 2021 for small colleges. After those years, the parabola turns down with the depth of descent being greater for small colleges. In either case, the coming sharp downward shift in the high school graduate pools after 2026 will have a profound effect on large and small colleges that will require them to take prudent measures very soon to preserve their financial resources. Since many small colleges are already at or near financial distress levels, then will need to act quickly in the next year to cope with massive losses in revenue.

Chart 3

Editorial Assistance by Jack Corby, Vice-President of Stevens Strategy