by Michael K. Townsley | May 26, 2024 | Economics and Higher Education, Financial Strategy and Operations

Pricing Power and Private Colleges and Universities

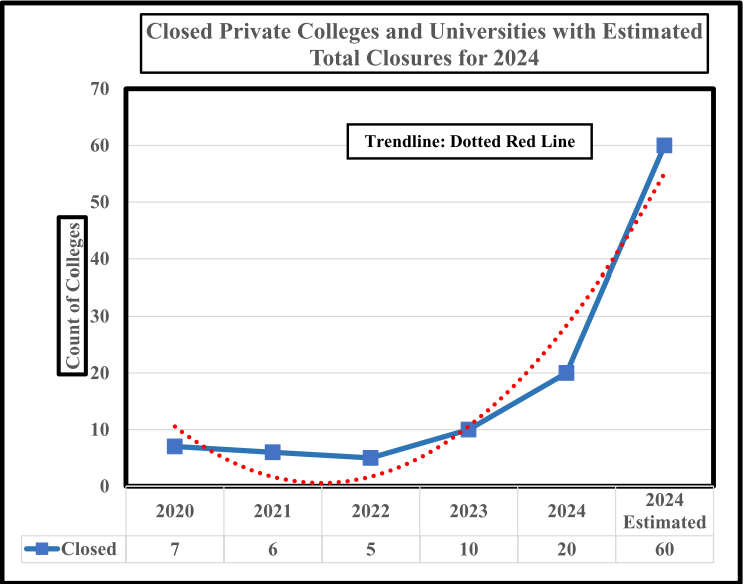

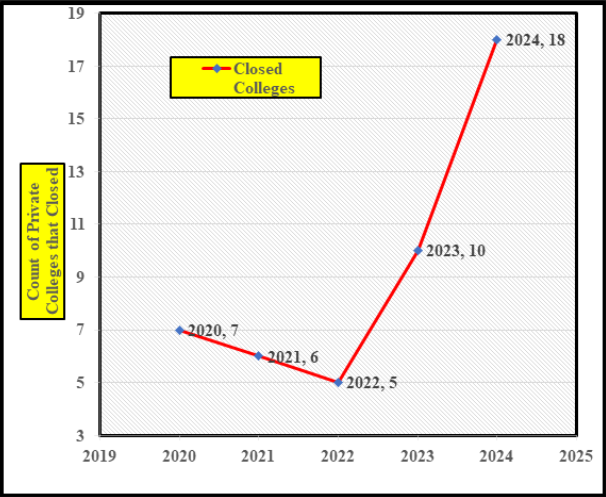

As of the first week of May 2024, Chart 1 shows that twenty private colleges have closed with a simple factorial estimating that sixty will close. The sharp exponential growth for 2024 does not bode well for many private colleges that are struggling to survive. Presidents and Boards of Trustees need to be cognizant of how tuition pricing decisions using ever-increasing tuition discounts to offset higher tuition prices can lead to contradictory or even unwanted effects on student decisions to enroll.

Chart 1

Current Financial State of Private Colleges and Universities

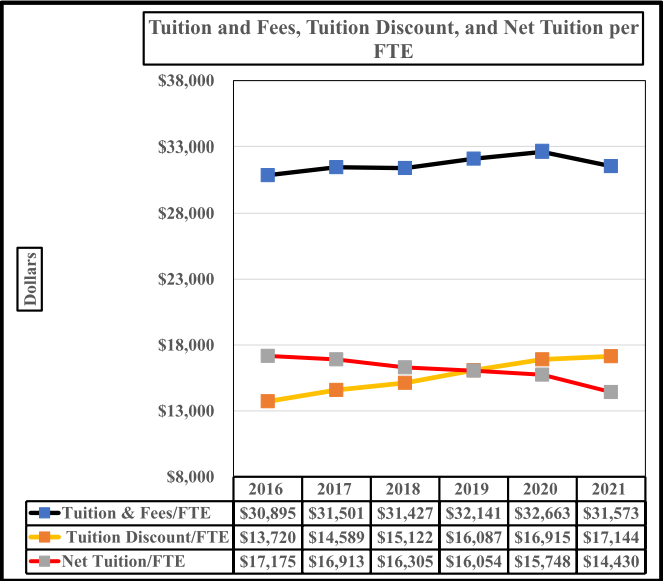

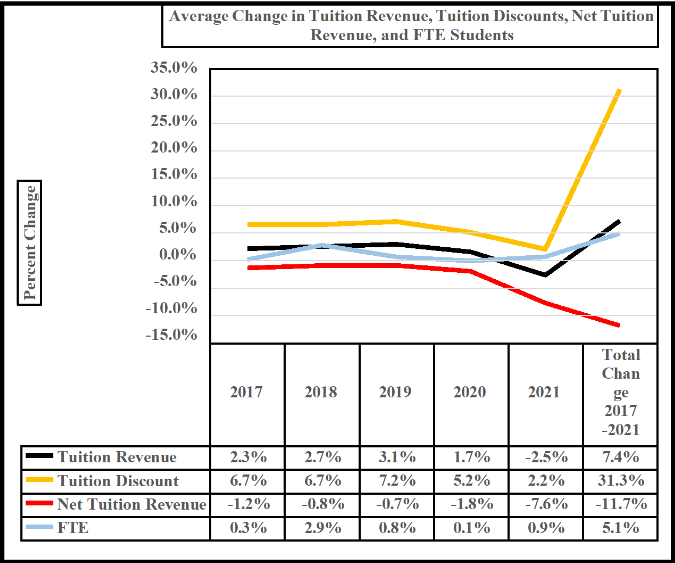

This paper now turns to what has happened with tuition pricing and the unintended consequences of those decisions over the past five years. Chart 1 and Table 1 adduce a major problem that has risen from tuition pricing decisions made by leaders of private colleges and universities. Chart 1

shows since 201: modest tuition and fee increases per FTE (full-time-equivalent student), an upward trend in average tuition discounts per FTE, and negative change in net tuition per FTE.

Dollars

Chart 1 indicates that the average net tuition per FTE crossed the average tuition discount in 2019, which suggests that from 2019 onward tuition discounts were exceeding the value of any changes in tuition and fees. If the past is a prelude to the future, more than likely tuition discounts will continue to increase after 2021. Because tuition discounts are unfunded by grants or endowment, they dot yield any cash benefit when they are increased. Unfortunately, tuition discounts diminish the amount of cash available to support on=going operational cash and force a college to draw cash from its unrestricted reserves.

Chart 2

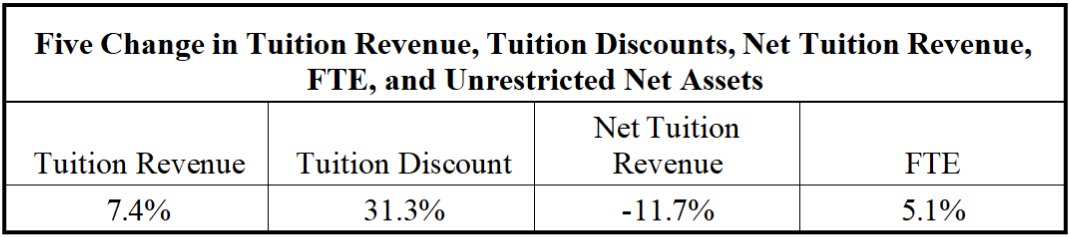

Table 1 shows the five-year change from 2017 to 2021 for tuition revenue, tuition discounts, net tuition revenue, and FTE enrollment. Although tuition discount was up 31.3%, FTE enrollment only grew 5.1%, while net tuition revenue fell 11.7%. Negative net tuition revenue means that there is less cash flowing from tuition revenue to support on-going operations. It is not unreasonable to conclude that these conditions contributed to an accelerated pace of private college closings. Based on closing data as of May 2024, the number of private colleges that closed was 100% higher than for calendar year 2023 and 150% greater than the average number of closings from 2020 to 2023.

Table 1

The failure of the tuition discount strategy to increase enrollment enough to offset lost revenue and cash has and will make it more difficult for presidents and boards of trustees to regain financial stability at many financially weak colleges. This paper uses basic economic theory to explain what shapes financial outcomes as colleges try to resolve their unstable financial conditions tuition and tuition discounts.

Conundrum of Tuition Pricing for Private Colleges and Universities

Before we start the discussion of tuition pricing, it would be useful to define several of the commonly used terms involved in tuition pricing and used to discuss tuition pricing decisions.

- Posted tuition and fees is the amount announced to the public for tuition and fee charges.

- Tuition and fee revenue is the amount of revenue received by the college from a student for tuition and fees; this figure is recorded in the accounting books and budget reports.

- Tuition discounts is an unfunded institutional grant that offsets a tuition and fee charge; these grants are recorded as expenses.

- Net price that the student pays after deducting institutional grants.

- Net price revenue is the net revenue recorded in the books that is paid by the student.

This paper uses basic micro-economic theory to explain tuition price setting. Theory posits that there is a price point where demand for a product or service and supply of that product or service are in balance. In balance means that at the price point the market for the good or service will be produced and purchased.

For private colleges and universities, demand is represented by a pool of students who file applications to one or more colleges. Supply comprises the colleges who offer enrollment in their majors to the student pool. Colleges competing for students are delineated by the choice set, which becomes evident when students file their applications. Therefore, the marketplace encompasses the student pool and their choice set of colleges. It is in this marketplace where the decision to enroll is at the intersection of the willingness of a student to accept and the price offered by a college.

Acceptance of an offer at a specific price is not necessarily at the tuition price advertised by the college. Typically, students and college agree on a net tuition price that is the amount the student owes after deducting a tuition discount. From the posted tuition. The discount is unfunded, that is, it is not supported by endowment funds. Since a tuition discount is unfunded, the college charges the discount to expenses and does not receive offsetting cash. However, a student may receive government grants or be awarded endowed scholarships that help a student pay for their net tuition balance.

Tuition pricing decisions is not simply a decision to accept a student at a given price, the college should take into account the price elasticity of the student pool, i.e.; student market. Price elasticity states that changes in price can have either a positive or negative effect on demand.

Elasticity generally operates as follows.

- If a market is elastic, price increases or decreases can have a significant effect on demand.

- If a market is inelastic, then price increases or decreases has little effect on demand, the demand.

- The price elasticity is: percentage change in quantity to the percentage change in price.

- If price elasticity is greater than 1, then price is elastic.

- If price elasticity is less than 1, then price is inelastic.

- If price elasticity is perfectly elastic; i.e.; a score of 0 or very near zero, then changes in price yield no changes in demand.

- Because elastic or inelastic markets can have a significant impact on the amount of product or service demanded, price elasticity can necessarily have an effect on revenue generated from sales.

Given the preceding statements on price elasticity and in the particular case of student demand, elasticity can have the following effects on tuition decisions:

- If the student market is elastic, then posted and net tuition increases or decreases can have a significant effect on the prospective student’s decision to enroll.

- If the student market is inelastic, then posted and net tuition increases or decreases has little effect on the prospective student’s decision to enroll.

- If the student market is perfectly elastic, then posted and net tuition, changes have little effect on the decision to enroll. (note reference for the preceding discussion can be found the Lumen Learning website).

Because price elasticity can have a positive, negative, or no effect on the decision to enroll, it follows that elasticity will directly affect tuition, net tuition revenue and the cash that flows from net tuition revenue.

Student Markets and Elasticity as of 2021

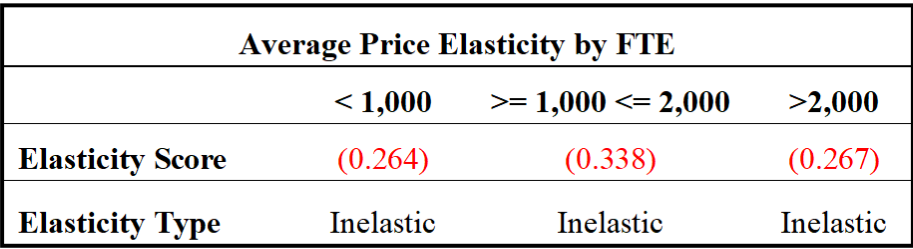

Now let’s turn to what the most recent data says about price elasticity in higher education and its impact on demand. Table 1 gives the price elasticity for three FTE enrollment groups (less than 1,000 FTE, 1,000 to 2,000 FTE, and more than 2,000 students). Price is inelastic in each group, which suggests that changes have little or no effect on enrollment decisions.

Table 2

The next table has the elasticity score and type for four risk rands. Each risk band (low, moderate, greater, and high-risk bands) represent a probability that estimates the chance of closing in the near future. The score range runs from 0.0 to 1.0 probability of closing for all four risk bands. All four bands are inelastic, as it was with the three FTE groups in Table 2.

Table 3

The elasticity scores of these two tables imply that tuition discounts will not generate sufficient net tuition revenue to offset the expense of the discount. Chart 3 illustrates the problem that the average private college must consider the impact of price elasticity when setting values for: posted tuition, tuition discount, enrollment forecasts, and budget revenue estimates. The charts indicate the average five-year changes in tuition revenue, discounts, net tuition revenue, and FTE enrollment as follows: tuition revenue was up 7.4%, tuition discounts grew 31.3%, net tuition revenue shrunk 11.7%, and FTE enrollment increased 5.1%.

As the preceding discussion on elasticity posits, and given that the average college is price inelastic, it should not be surprising that the average college did not generate enough new student revenue to offset the cost of the tuition discount.

The findings on elasticity and net tuition revenue suggest that tuition discount strategies are not the way to go, if a president and board want to avoid joining the colleges in Chart 1 that have fallen off the cliff. Other places where the leadership could focus its efforts would be: cost cutting, new programs, merger, and not waiting until the last minute to solve their financial problems. If there is one aspect that many closed colleges have in common is that they waited too long to figure out a new strategy. Another common mistake among presidents in looking for solutions is that they talk with other presidents who have the same problems and also do not have workable ideas to stop the rush to the edge of the cliff.

Chart 3

There is one last note about pricing and that is pricing power in the marketplace. Pricing power is evident when a specific institution can set the posted and net tuition price and other college follow in their pricing strategies. Those institutions would be called price makers. While the price follower institutions are called price takers. The later have very little control over their pricing strategies. The price taker must like the above comment about inelastic pricing failures over the past five years, must focus over other areas to improve their capacity to compete and survive in the higher education market.

by Michael K. Townsley | May 26, 2024 | Private Colleges & Universities in Crisis, Strategic Planning

Zombie Colleges are the walking dead of private colleges. They have: no cash, cannot make payroll, pay bills or debt services, violated their debt covenants, and only a few faculty who work for nothing. [1] The Sisyphean hill for these colleges is very high and difficult to climb

because they often have lost their accreditation. Yet, they still try to recruit students. Zombies are the classic example of ‘caveat emptor’.

The simplest way to find Zombies is to look for private colleges that have reported negative unrestricted net assets (the assets that hold mostly funds for on-going operations – payrolls, payables, debt service).

Table 1 is a five-year report on Zombies with 2021 as the last year. There were nineteen

colleges reporting negative unrestricted net assets over the five-year period. Eleven of those

colleges had a negative change in enrollment for the period. There price elasticity was less than one, which means that changes in tuition discounts had little or no effect on enrollment. For

those colleges to get any increase in enrollment, they had to offer a tuition discount of 81.8%. So, if they did have increased enrollment, those colleges only received 20 cents in cash from a dollar of tuition revenue. These huge discounts explain why they were not able to escape their

doomsday collapse.

Table 1

| Zombie Colleges – Five Year Report |

| Negative Unrestricted Net Assets for 5 years |

Elasticity for Last Year |

Tuition Discount for Last Year |

Negative Change in FTE for 5 Years |

| 19 |

0.41 |

81.8% |

11 |

The nineteen colleges were diving into Zombie oblivion at a time when the government dropped huge piles of pandemic largess to keep colleges alive. Well, they may not be alive, but they are

still there despite being Zombies bringing in students and providing unknown educational services for them. These colleges cannot survive long on a no cash and no accreditation

regimen. Typically, the end comes when the U.S. Department of Revenue no longer permits the college to issue federal financial aid to students. Then the Zombie colleges joint the Zombie

march to the Zombie Cemetery singing – Ha! Ha! Ho! Ho! Here we go to haunt our Lemming friends as they follow us to the Zombie Boneyard!

Reference

1 Quintana, Chris (I May 9, 2024) (Retrieved May 10, 2024);” Zombie Colleges? These universities are living another life online, and no one can say why”; USA Today; Zombie

colleges? These universities are living another life online, and no one can say why (msn.com).

by Michael K. Townsley | Apr 6, 2024 | Financial Strategy and Operations, Private Colleges & Universities in Crisis

Michael Townsley, Ph.D.

March 31, 2024

Introduction

For the past decade, our colleagues and columnists have remorsefully muttered about friends in terminally ill colleges. Now, we know “for whom the bell tolls.” As more old colleges are thrown on the death cart, other small colleges only wait and wonder if their college is next to be chucked on the heap of history.

College closings have accelerated since 2022 despite the large influx of federal funds in 2022 (see Chart 1). What is particularly troubling for 2024 is eighteen colleges have announced that they are closing or closed in just the first three months. This is twice the average for the previous four years. If that trend continues, seventy-two private colleges could close by December 2024.

Chart 1[1]

Count of Private Colleges and Universities that Closed between 2020 and March 2024

Seemingly, COVID funding may have masked financial problems that reappeared as the funds were depleted. Here are several problems, given current conditions in the private higher education market that could have an adverse effect on the financial vulnerability of a college:

- Long-term decline in births and by extension smaller high school graduation classes.

- There is no single demographic on the horizon that can provide a large number of new students as there were starting in the 1980s, when women either returned to finish a degree or working women saw opportunities that a degree would provide.

- When the pool of buyers shrinks, economics posit that prices will decline and either demand will increase or supply will decline, thus colleges will close. Prices, in this case tuition, are cut by increasing the tuition-discount rate. NACUBO (National Association of College and University Business Officials) reported that in 2023 the discount rate was 56.2%.[2] As discounts rise, tuition produces less cash, which reduces the amount available for expenses. Tuition discount increases coupled with less cash from tuition is worrisome for tuition-dependent colleges and universities. Because the average discount rate was 56.2% in 2023, the average private college received ess than 50 cents on the dollar from tuition revenue. Several news items note several colleges are offering discounts up to 65% of tuition (this rate does not include discount rates offered by highly selective colleges and universities).[3]

- Some colleges continue to retain academic programs with too few students and too many faculty and staff, while other colleges are eliminating programs to reduce costs. (See this reference: “How US Colleges Are Responding to Declining Enrollment”.[4]

- Colleges are expected by governmental regulators to moderate rates of attrition, Therefore, low academic skills of entering students force colleges to expand academic support services at significant cost to minimize attrition. (See these references for articles about skill: “Student achievement gaps and the pandemic”[5]; “The pandemic has had devastating impacts on learning”[6]; “Math Skills Fell in Nearly Every State”[7] “High School Students Think that They are Ready for College, But They Aren’t”[8]

- Owing to declining enrollment, some colleges carry empty rooms and buildings on their books Although these rooms and buildings are not used, they still drain resources as they need custodial care and regular maintenance, otherwise the unused building could become a safety hazard.

- Maintaining and operating out-of-date IT equipment and software reduces the capability of a college to serve its students, manage its finances, and efficiently run academic and administrative software. Since these colleges may not have the resources or the good fortune to receive grants or gifts for new IT technology, they will lag behind better-funded competition and be less attractive to new students.

Vulnerability Gauge – Predicting Financial Risk

This paper introduces a Vulnerability Gauge to predict if a private college or university is or is not at risk of financial failure. A logit regression tested the model with several different combination of variables. The model was applied to a random sample of forty-four private colleges and universities drawn from the Integrated Postsecondary Education Data System (IPEDS). database. The tests found the most robust and parsimonious model had an 86.3% prediction rate of financial risk when these two factors were used:

- Annual percentage change in unrestricted net assets over five-years (for most private colleges, these assets represent the ready financial reserves that cover operational expenses);

- The total change in FTE (full-time enrollment) over five-years.

The logit regression yielded probability of financial failure for each school in the sample. The probabilities were then arrayed into four risk bands: low, moderate, greater, and high risk of financial failure as shown in Table 1. The risk bands indicate that the lower the probability, the lower the risk of closing and the higher the probability, the greater the risk of closing.

Table 1

Risk Bands of Probabilities for Study Sample

Findings from Large Sample Analysis of Unrestricted Net Assets and Enrollment

After the random sample was tested, the model was then employed to test the vulnerability of 949 private colleges that were open in 2016. This sample excluded medical schools, research institutes, arts programs, seminaries, and other specialty colleges. The analysis covered the period 2016-17 to 2021-22, which was the most recent year in which IPEDS higher education data was available.

Chart 2

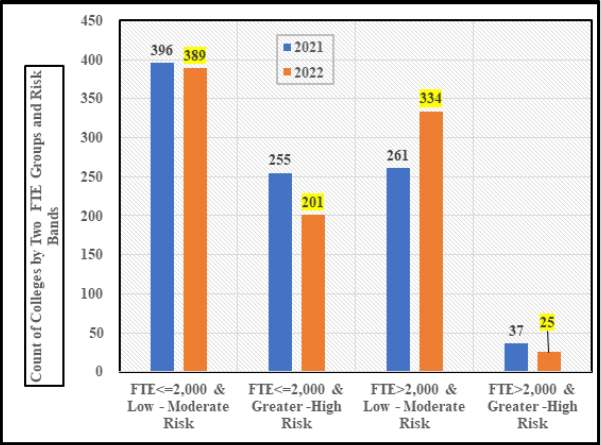

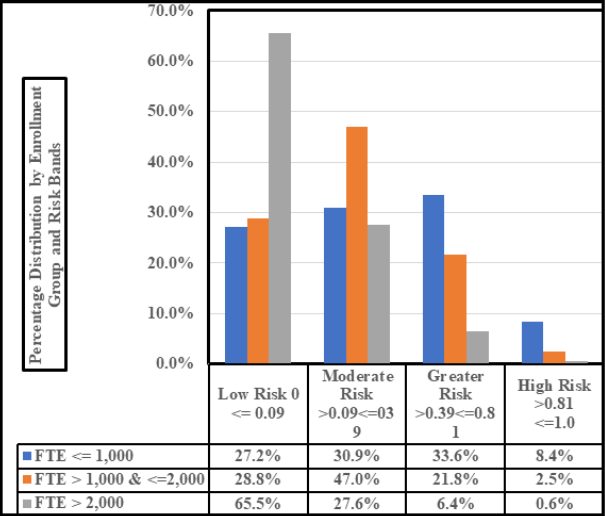

Colleges Assigned to Two Classes of Risk and Enrollment for 2021 and 2022

Chart 2 compares colleges based on their risk band and enrollment (FTE) for the years 2021 and 2022. Two major variables are displayed in the Chart – FTE enrollment and Risk Bands, which are described in Table 1. The FTE is divided into two categories of colleges, FTE with less than or equal to 2,000 students and FTE with more than 2,000. The second variable merges Risk Bands. The first risk band includes colleges with low to moderate Vulnerability Guage scores of ‘0 to less than 0.39’ and the second includes colleges with greater to high-risk scores greater than 0.39 to 1.0.

Here are several observations from Charts 2:

- In 2021, 255 private colleges with less than or equal to 2,000 students were rated at greater to high risk, but only 37 colleges with more than 2,000 students were rated with the same risk. In other words, institutional size seems to be a major factor in determining risk. In 2021, the risk rating for small colleges was 6.9 times greater than for larger colleges.

- In 2022, 201 more smaller colleges than larger rated as greater to high risk, 54 fewer colleges than in 2021. Yet, the greater to high-risk rating for smaller colleges was 8.0 times larger than larger colleges.

- In 2022, the enrollment group with more than 2,000 students saw seventy-three more colleges rated as low to moderate risk, in comparison to 2021, but this group had twelve fewer colleges rated as higher to greater risk.

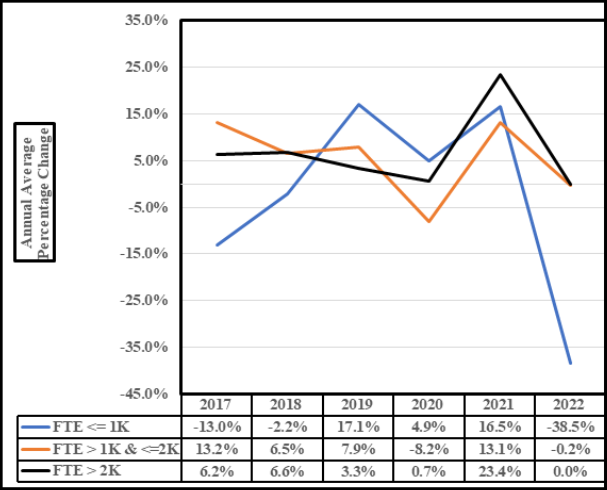

Chart 3 includes the same enrollment and risk groups as in Chart 2, but includes the average percentage change in unrestricted net assets for the years in the 2016-17 to 2021-22 period.

Chart 3

Average Percentage Change in Unrestricted Net Assets for Colleges Rated as Low, Moderate, and Greater Risk from 2016-17 to 2021-22

What is interesting about this chart is the instability from year to year in unrestricted net assets, some years rising and others falling . When unrestricted net assets fall into negative percentage changes, it usually means the college is reporting deficits for the year. For private colleges with small endowments, serial deficits could threaten the financial survival of the college.

Chart 3 indicates that the full effect of federal pandemic funds did not appear until 2021, when each enrollment group in our study had an increase in unrestricted net assets Nonetheless, in 2022, the three enrollment groups experienced sharp declines in unrestricted net assets, and small colleges had the largest decline (-38.5%).

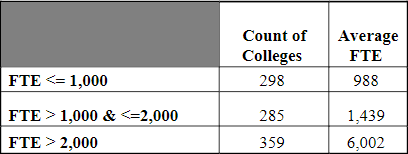

Chart 4 presents a different look at the distribution of colleges by enrollment group and risk bands. It confirms that risk follows scale of enrollment with small colleges facing the most risk of financial failure. According to IPEDS data, small colleges rated as greater to high risk have on average enrollment of 1,200 students.[10]

Chart 4

Distribution of Colleges in Research Set by Enrollment (FTE) Groups and Risk Bands

The relationship of size and vulnerability for private colleges and universities should not come as a surprise, because most private colleges are tuition dependent. Small tuition dependent colleges are especially vulnerable. There are several issues that make the economics and finances of small colleges problematic:

- Recall this quote from Ernest Hemingway’s masterpiece, The Sun Also Rises, “How did you go bankrupt?” Bill asked. “Two ways,” Mike said. “Gradually and then suddenly.” Small colleges often lack the financial flexibility when price competition is intense (i.e., tuition discounts, as reported by NABUBO studies), leading to smaller and smaller yields from tuition enrollment.

- Breakeven price rises owing to accreditation, governmental requirements, and student expectations tend to increase fixed costs, which will increase breakeven prices due to the small number of students available to cover fixed costs. The chief financial officer and marketing office must then increase tuition discounts to remain competitive. Here is where the dilemma arises for the chief financial officers at tuition dependent colleges: Rising tuition discounts diminishes the flow of cash from tuition revenue. Less cash from tuition means that there may be insufficient cash to cover expenses. Under this predicament, these colleges lose twice – they have insufficient net revenue to cover expenses leading to a deficit, and cash reserves shrink because cash flow from revenue does not replenish reserves. As noted above, serial deficits can run the college into the ground.

Table 2[13]

Number of Colleges and Average FTE for Each Enrollment Group

Conditions Unique to Higher Education that Degrade Response to Risk

Before any remedy can be prescribed, we need to understand why so many private colleges are slow to respond to economic and financial threats to their existence. The list at the start of this paper identified several factors that shape financial stress, but there are further internal and operational issues that also shape the financial vulnerability at small private colleges. See the following list of issues that may foster financial stress.

- Contradictions of dual governance, where major academic financial problems, and their solutions may be stymied by conflict between the manner in which faculty and administrative govern their respective areas.

- Faculty tenure that places costs, sometimes substantial, for the dismissal of faculty due to a major reorganization and the termination of academic majors or programs.

- Explicit and implied contracts with students, faculty, and external partiesin student handbooks that sets out the liability to students when programs, athletic programs student services, or dormitories are ended or downsized, faculty handbooks that specifiy work conditions, alumni traditions that carry costs, or unstated relationships with local governments that have inherent costs.

- Accreditation and governmental regulations that may stipulate financial conditions to sustain operations and standards for academic programs and student services that can a) raise the cost of operations and b) make it difficult to change academic programs. Governmental regulations can also stipulate financial conditions and standards for maintaining eligibility for federal funds or for compliance with federal mandates.

- State Non-Compete Regulations can keep a college from offering a new program if another institution already offers it.

- Human Capital, buildings and equipment may not match what a college needs during a strategic reorganization to better serve its student market while reducing costs.

Besides the preceding organizational failures, leadership failures by the president and board of trustees shape a private college’s capacity to rapidly respond to financial crisis and building financial vulnerability –. For the last ten years, top leadership at fiscally and operationally stressed private colleges have unintentionally exacerbated problems until a college collapses and closes. Salient characteristics of the leadership failures include:

Presidents

- Risk aversion, when dealing with fundamental changes in student and job markets;

- Tendency to substitute platitudes for real hard-nosed planning

- Not understanding that there are no new student markets, as there were in the eighties and nineties, when women and minorities enrolled in ever-larger numbers;

- Not recognizing that time is short for action and resources are quickly being depleted by every passing day.

Boards of Trustees

- Trustees may not invest either the time or energy to understand the perilous condition of their institution.

- Trustees, in some instances, may not have policy-making or management experience.

- Trustees may be unwilling to challenge claims made by the administration that all is well despite contradictory and obvious evidence.

- Trustees too often do not take the financial problems of the institution seriously until they like the president discover that the college has too few resources and very little time left.

- The Board may not fully appreciate its culpability for failing to oversee and preserve the resources of the institutions for future generations of students.

Potential Remedies for Reducing Financial Risk

Responding to the highest level of financial risk first requires information that delineates the financial, operational, and market conditions of the institution. Before diving into strategic and operational turnaround strategy, the president and board need to acknowledge whether or not operational deficits have become a recurring and increasing threat. In the next step, both the board and president need to know the level of financial reserves currently available, whether those reserves are expanding or shrinking, and how long those reserves will last, if there are operational deficits.

After the board and president fully agree that the college is at risk of financial failure, the board should arrange for a third party to evaluate the college’s – financial condition, in particular, cash flow; academic program contribution to financial performance; the connection between labor markets and academic programs; and the expectation of the student market. There is no surer sign of performance inefficiency than a major with three or more full-time faculty instructing four students in a major.

It is imperative for recognize that Boards need to support Presidents who lead with fortitude, intelligence, and foresight, otherwise it will be difficult for the institution to withstand conflict generated by internal and external dissension in response to major strategic changes. Conflicting solutions and dissension could become a regular event. Nonetheless, every day lost, before taking steps to overcome the inertia toward failure, will push the college closer to its demise.

Since time is of the essence, the board and its president must press-on with dispatch the president, faculty, staff, and administration moving forward while not letting precious time be excessively expended on internal politics and lack of follow-through. Of paramount importance in a survival turnaround is never losing a marketing season for new students. If that happens, the college could lose a year out of the precious short-time available to avoid financial failure.

The factors that make-up the Vulnerability Gauge can guide the development of an effective strategy to generate larger and positive net incomes that increase unrestricted net assets. Focusing on factors in the Vulnerability Gauge will lead to optimizing markets, generating higher cash flows from tuition, cutting administrative expenses, improving the financial and operational relationship between faculty and students, imposing controls on the operational efficiency of capital investments in grounds, buildings and equipment, and moving revenue generating centers toward positive contributions to the bottom line.

For colleges that have arrived at the brink of survival, there seem to be three strategic options that colleges at the brink of extinction consider:

- Merger

- Forming a partnership;

- Looking for wealthy alumni or local donors.

Usually, none of these three strategies are successful. The main reason is that colleges in dire straits have nothing to offer but debt, large financial liabilities, tenured faculty, unusable assets, law suits, and unhappy students and alumni. For the college being petitioned to help failing college, the best option may be to let it fail and pick up the pieces at a discount. The sad aspect of the current spate of college closings is that the causes for a particular institution may be beyond the control of its leaders. Over the next decade, private colleges and universities may operate in a different form and serve student markets with different characteristics, expectations, and capabilities.

Summary of the Main Points about the Vulnerability Gauge

The Vulnerability Gauge was developed as a tool for presidents, boards of trustees, and other interested parties to estimate the risk of financial failure for a private college.

- As noted above, colleges with enrollments of 2,000 or fewer students operate at a greater to highest level of risk. As is evident from news reports over the past several years, this group is shedding the most colleges. Small colleges have difficulty sustaining operations in a high-risk environment.

- The main issues threatening the survival of small, high-risk private colleges are: a shrinking pool of new students, the inflationary costs of operations, ever more stringent governmental regulations, and the loss of confidence by a growing number of high school graduates that a college degree may not be worth the cost.

- The Vulnerability Guage predicts the level of risk that a private college faces. It estimates financial risk using FTE enrollment and the change in unrestricted net assets. It also offers strategic entry points through the factors that are part of Guage.

- For the 201 small colleges living on the brink of survival, there is no timeto dawdle, action must be taken swiftly.

Reference

-

Higher Ed Dive Team ( March 11, 2024), “How many colleges and universities have closed since 2016”; Higher Ed Dive; How many colleges and universities have closed since 2016? | Higher Ed Dive. ↑

-

Moody, Josh (April 25, 2023); “Tuition Discount Rates Reach New High”; Inside Higher Education; NACUBO study finds tuition discount rates at all-time high (insidehighered.com). ↑

-

Some Colleges that Offer the Biggest Discount Rate; NICHE; (Retrieved March 26, 2023); Colleges That Offer the Biggest Discount – Niche Blog. ↑

-

Downes, Lindsey, editor (July 28, 2023) (Retrieved March 27, 2024); “How US Colleges Are Responding to Declining Enrollment”; WCET Frontiers; How U.S. Colleges and Universities are Responding to Declining Enrollments – WCET (wiche.edu). ↑

-

Student achievement gaps and the pandemic (Retrieved March 27, 2024); (Retrieved March 27, 2022); CRPE Reinventing Public Education; ED622905.pdf. ↑

-

Kuhfield, Megan, Jim Soland, Karyn Lewis, and Emily Morton (March 3, 2022) (Retrieved March 25, 2024): The pandemic has had devastating impacts on learning”; Brookings; The pandemic has had devastating impacts on learning. What will it take to help students catch up? | Brookings. ↑

-

Mervosh, Sarah and Ashley Wu (October 24, 2022) (Retrieved March 27, 2024); “Math Scores Fell in Nearly Every State and Reading Dipped on National Exam”; New York Times; Math Scores Fell in Nearly Every State, and Reading Dipped on National Exam – The New York Times (nytimes.com). ↑

-

Heubeck, Elizabeth (February 21, 2024); (Retrieved March 27, 2024); “High School Students Think that They are Ready for College, But They Aren’t”; Education Week; High School Students Think They Are Ready for College. But They Aren’t (edweek.org). ↑

-

IPEDS (Retrieved March 1, 2024); Complete Data Files; IPEDS Data Center. ↑

-

IPEDS (Retrieved March 1, 2024); Complete Data Files; IPEDS Data Center ↑

by Michael K. Townsley | Mar 30, 2024 | Private Colleges & Universities in Crisis, Strategic Planning

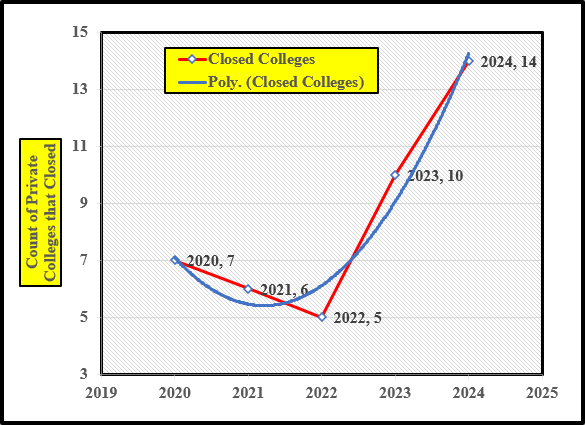

The higher education market is shedding colleges at a record pace. Despite the large influx of federal funds in 2022 to offset the effect of the pandemic (see Chart 1), fourteen private colleges closed or disappeared in mergers during the first three months of 2024. If this trend continues through 2024, there is a good chance that fifty-six private colleges will have closed their doors by December. Apparently, COVID funding may have only been a short-term reprieve for private colleges in higher education.

Chart 1 ([1])

Count of Private Colleges and Universities that Closed between 2020 and March 2024

(The blue trendline is a second order polynomial)

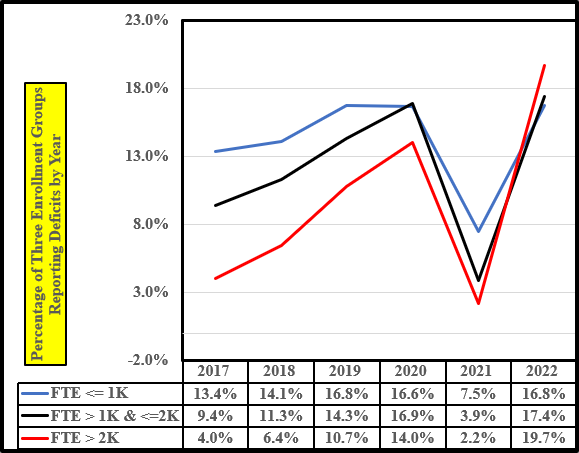

Operational deficits for the years 2017 to 2022 indicates that private college and universities were under financial stress prior to the pandemic funding, and many of these colleges are returning to a state of stress. Chart 2 shows the percentage of private colleges reporting operational deficits by year from 2017 to 2022 for three FTE (full-time-equivalent students) groups; colleges with enrollments: less than or equal to 1,000 FTE; between 1,000 FTE and less than or equal to 2,000 FTE, and greater than 2,000 FTE.

Each enrollment group had increasing percentage of deficits between 2017 and 2021 except for the smallest enrollment group. The latter group had a small decline in deficits between 2019 and 2020. In 2021, the percentage of deficits plummeted as pandemic funds reached colleges. Nevertheless, in 2022, the percentage of colleges with operational deficits shot up to their highest level. If the 2021 dip is removed, the percentage of deficits returned to the pre-2021 trend. The exception was colleges with more than 2,000 FTE, where deficits jumped to a rate higher than the other two groups of private colleges. There is no ready evidence of why this occurred; unless larger colleges were making large expenditures and had the reserves to strengthen their IT support given their experience during the pandemic.

Chart 2 ([2])

Percentage of Three Enrollment Groups Reporting Deficits between 2017 and 2022

Here are several observations derived from the Charts 2 and the following Chart 3.

- Private Colleges with enrollments less than 1,000 FTE have the most difficulty in generating positive income annually Table 1, (Charts 2 and 3).

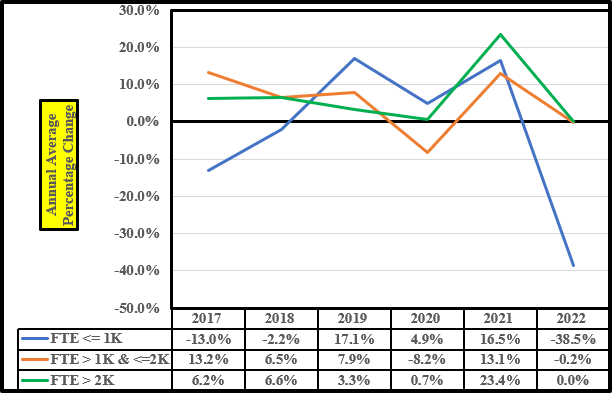

- Annually small colleges, on average, generated a 2.5% operational deficit (Table 1). The danger sign for these colleges is that their annual operational deficit leapt to 38.5% after COVID funding (see Chart 3).

- The middle FTE enrollment groups seems to be living the life of a porpoise running above and below the surface of operational net income. Their average operational net for the five-years was 5.4% (Table 1). Yet, in 2022, 17.4% of these colleges disclosed deficits (Chart 1). This group will bear watching over the next several years.

- The largest colleges with FTE greater than 2,000 students is the most perplexing. It’s average annual net for the five-years was 6.7% (Table 1), which was only 1.3% greater than the middle group. For 2022, the annual net for large private colleges was 0.0%, which is not very spectacular. Also, this enrollment group had the largest proportions of its institutions reporting deficits in 2022 (Chart 2). One might infer that this enrollment could possibly have financial reserves to power forward despite annual deficits. Even so, if some of these large colleges assume that a series of deficits will not endanger their financial viability, they could be whistling past the graveyard.

Table 1 ([3])

Average Annual Operational Net Income for Three Enrollment Groups of Private Colleges

CHART # 3 ([4])

Average Annual Net Income for Three Enrollment Groups from 2017 to 2022

Conclusion

As is evident from the preceding table and charts, this is a perilous time for many private

colleges and universities. Survival at deficit entangled colleges will depend on strong management by boards of trustees and presidents. Difficult and often painful decisions will have to be made if an institution intends to survive. If financially vulnerable colleges fail to act in a timely fashion, they may well end up on Chart 1.

References

-

Higher Ed Dive Team ( March 11, 2024), “How many colleges and universities have closed since 2016”, How many colleges and universities have closed since 2016? | Higher Ed Dive; Higher Ed Dive Team; Higher Ed Dive. ↑

-

Financial Data, Integrated Postsecondary Education Data System (Retrieved March 2024) https://nces.ed.gov/ipeds/; ↑

-

Financial Data, Integrated Postsecondary Education Data System (Retrieved March 2024) https://nces.ed.gov/ipeds/; ↑

-

Financial Data, Integrated Postsecondary Education Data System (Retrieved March 2024) https://nces.ed.gov/ipeds/;

Originally published In StevensStrategy.org ↑

by Michael K. Townsley | Sep 19, 2023 | Private Colleges & Universities in Crisis, Strategic Planning

First Published on Stevens Strategy Blog

Nearly every week news flashes a report of another private college either closing or in deep financial trouble. Here is a short but not exhaustive list of colleges that have closed this year: Alderson Broadus, Cardinal Stritch, Medaille, Presentation College, Bloomfield College, Holy Name University, Iowa Wesleyan, Cazenovia College.

There are also troubling signs with the number of presidents who are suddenly leaving colleges, some have reportedly been employed for less than a year. We do not know the reason, but it is not a favorable sign when a college’s new leader suddenly resigns.

Many blame deep structural problems. Literally translated, they are saying they are not enrolling enough students and they cannot afford the fixed costs of delivering degrees or serving students, such as: tenured or long-term contracts, athletic programs, support services or debt-service on buildings

Rick Seltzer in the August 2nd Chronicle of Higher Education Newsletter, referencing Ernest Hemingway, said this about Alderson Broadus’ sudden closure” You go bankrupt, Hemingway wrote, “gradually, then suddenly.”

The question for many small, tuition-dependent private colleges are they beginning to hear the bells tolling for their future? If you are hearing the creak of the ropes in the bell tower, here are several steps that can be taken:

- Determine, how much cash, your institution needs to survive for five years.

- If you are not going to have enough cash to survive, identify revenue-expense flows that are out-of-balance (i.e.; where reliable revenue sources are not covering each major expense outlay); the president and board of trustees must agree that:

- The cash prognosis truly represents the cash position of the instituion and demands immediate strategic action;

- The president must inform the board of the strategic action plan;

- The board either agrees to affirmatively support the plan or needs to find a new president.

- These steps can determine strategic plans by identifying:

- Reallocation of endowment assets and seeking out donors to create a cash reserve for new strategic action;

- New sources of revenue that can provide substantial new revenue flows (i.e.; find new markets that can be easily and quickly entered without an excessive cash outlay).

- New academic programs and redesign existing programs so that they efficiently lead to future income for graduates sufficient to cover their life goals and educational loans;

- Instructional programs that are not operating efficiently and either restructure them or close them; examples abound such as: programs with full-time assigned to work with only a few students or programs that are no longer relevant to the job market;

- Student support services that do not reducing attrition rates;

- Athletic teams that do not generate sufficienty net tuition revenue to cover the cost of their operation and attendant administrative costs;

- Plant assets that add to operational costs without generating direct benefits to the mission of the college. orthe operation of the college like: empty dormitory space, other empty buildings., or buildings with a large number of empty rooms. The board and president need to divest the college of burdensome assets.

- While the preceding steps lay the framework for survival, they are only valid to the extent that a president is willing to use these steps to come to grips with the deteriorating financial condition of the college. President’s lead a college out-of- to quickly assess academic costs and weakness in serving its market. Additionally, a president needs the political skills to know where and how to respond to conflict so that action is not bogged down by the governance merry-go-round. Moreover, these presidents must have the drive to lead and to get their hands dirty.

Presidents of struggling colleges must act quickly because the turnaround plan has to be fully-in-effect within two years given the current pace of financial distress. There can be no dawdling; they must carry the action forward. Last but not least, the Board either supports the president or the president must leave. The longer that action is delayed, the greater the chance that they will lose the most important commodity needed for survival – the time to emplace effective changes. If the leaders take too long, they will lose the race to survival.